Robinhood, is a U.S.-based financial services company headquartered in Menlo Park, California. The company is a zero-fee trading platform in shares and ETF listed on U.S. stock exchanges through a smartphone mobile app.

Robinhood is particularly attractive to the so called millenials, people born between the 1980s and 2000s years. Of the 150,000 accounts that signed up before Robinhood's official launch in 2014, 75% were born in 1980 and later.

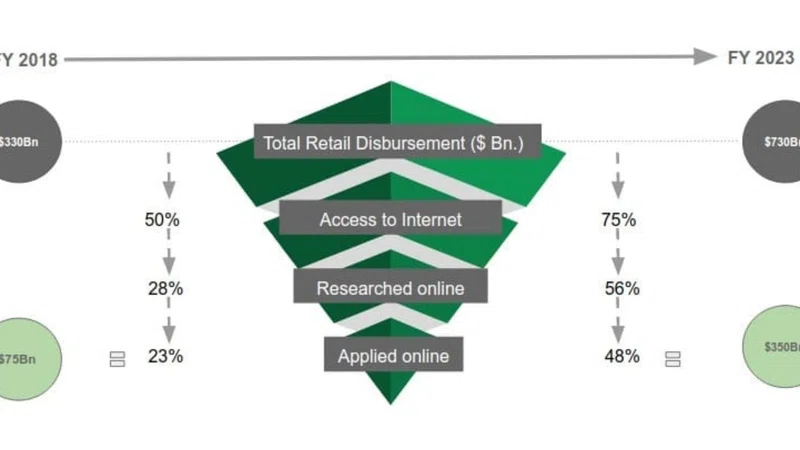

Robinhood accounts growth

Robinhood was particularly attractive to millianials for two main reasons:

- zero trading commissions vs. 5 -10 dollars required by the main online brokers;

- no initial deposit minimum for Robinhood’s standard account vs. a account minimums run anywhere from $500 to $1,000 required by the main online brokers.

The growth experienced by Robinhood in the last few years was extraordinary, from 0 to $ 5.6 bn in just 4 years.

Robinhood Checking & Savings accounts

To keep up with the growth, Robinhood decided to disrupt the traditional US savings market. In mid-December 2018 announced that it will offer 3% interest rate on its accounts called Robinhood Checking & Savings accounts,, a sky-high payout in today’s low-rate environment. This move is aimed at attacking the traditional banks in their core business, which is the traditional banking business of saving and checking accounts.

Regtech: SIPC vs. FDIC protection for online deposits

Robinhood move was done not paying enough attention to regtech details.

Robinhood Checking & Savings accounts are backed up to $250,000 by the Securities Investor Protection Corporation (SIPC), an organization that insures funds held at broker dealers. This is different from the Federal Deposit Insurance Corporation (FDIC), the federal agency backed by the full faith and credit of the US government.

In the case of default the regulation applied to Robinhood deposits (SIPC protection) is different from the one applied to deposits of traditional banks (FDIC protection).

SIPC protection is limited. SIPC only protects the custody function of the broker dealer, which means that SIPC works to restore to customers their securities and cash that are in their accounts when the brokerage firm liquidation begins.” SIPC acts to recover the money the depositor lost in case of broker’s failure.

Instead FDIC insures deposits in member banks up to US$250,000.

In the event of a bank failure, the FDIC pays insurance to the depositors up to the insurance limit. The FDIC assumes the task of selling/collecting the assets of the failed bank and settling its debts. No depositor has ever lost a penny of insured deposits since the FDIC was created in 1933.

Very recently SIPC President said he has serious concerns about the plan and that SIPC protects money with a brokerage firm that is used for the purchase of securities. Deposit for any other purpose are not protected.

Conclusions

The launch of Robinhood Checking & Savings accounts was:

1) a great idea to disrupt the savings market;

2) a bad idea the way it was implemented.

The management was too eager to launch the product without talking to regulators.

They thought it was a great idea and they launched the product right away.

All at sudden the company scrubbed the page from its website and issued a blog post explaining the change calling it a “cash management” service.

That was too much rush at the beginning and too much rush at the end of the launch.

You lose credibility with this kind of behavior.

It is true that young entrepreneurs think they can do things fast.

But it is also true that if you launch a product and the next day the product is withdrawn without any explanation people might think the company is too volatile.