When fintech first became a ‘thing’ there were industry rumblings about upstart startups seeking to disrupt the market, with an eye to replacing banks and insurers. There was a view that all the things which a bank or insurer does could be done better and cheaper by a technology-powered fintech. And there is still some suspicion in the market today. So, is fintech the friend or foe of the established industry?

How the relationship between fintechs, banks, and insurers has evolved

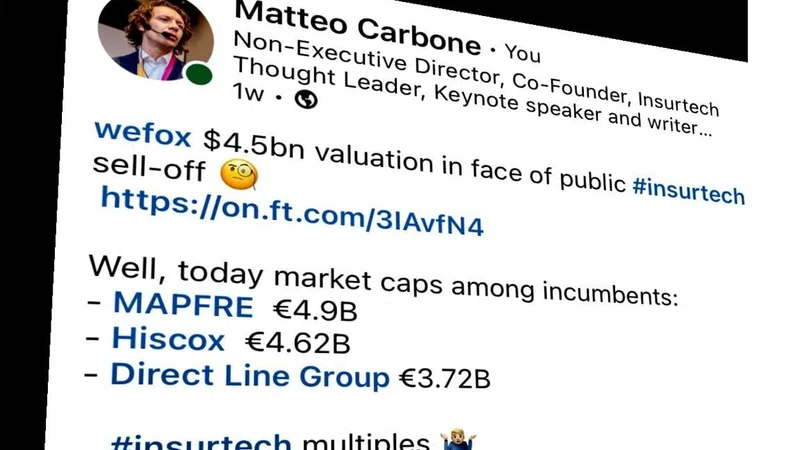

To gain a clear view of the relationship between fintechs, banks, and insurers, it makes sense to separate the sectors. Because the value proposition of fintechs and insurtechs are slightly different.

While new European insurtechs seem to have been popping up like mushrooms in the last 3-4 years, only a handful have applied for insurance licenses. The others have instead focused on their own part of the value chain, whether that is distribution or product underwriting and administration. Their primary aim is to work with traditional insurers or the reinsurers who sit behind them.

The result of this has been that part of the insurance value chain has shifted from incumbents to insurtechs, and this will continue as they continue to grow their market share. However, there is still an important (and profitable) role for insurers as they are the ultimate holders of risk capital and get remunerated for managing their portfolio of insurtech relationships well.

In banking, the story is at least partly similar. Few fintechs have applied for full banking licenses, with most following the electronic money institution (EMI) model. This means that while these fintechs can process payments and hold customer funds, those funds must be ‘safeguarded’ by a regulated bank. Only regulated banks are allowed to accept deposits and lend them out for a margin.

However, as the share of the banking and payments value chain available to fintechs is significantly greater than for insurtechs, they do still represent more of an existential threat in this sector. So, what might the future hold for all three parties?

Is collaboration key to the UK remaining at the forefront of fintech?

In insurtech, collaboration has become the established form and this is not likely to change. As the sector develops, it is contributing an increasing amount to the insurance industry, assisting in streamlining and extending the services of insurers. It is a mutually sustaining relationship, and there is little need for insurtechs to take their own path and compete against the established insurers.

In the case of fintechs and banking, however, in the long term, it seems unlikely that banks will be able to thrive just by collaborating with fintechs. Ultimately, they will need to retain ownership of important parts of the value chain – such as making credit decisions and processing payment transactions. This means that they will need to either build fintech-style capabilities in-house, or acquire fintechs. And you can already see this happening among the more forward-looking banks, who are pursuing both strategies.

Fintech and insurtech are some of the fastest growing sectors and they are evolving rapidly. For the insurance industry, this is only a positive move, bringing new services, cost savings, and better underwriting. But for the banking sector, the situation is less straightforward. Collaboration has created a successful business model for many, but the likelihood of direct competition is greater: many fintech brands will ultimately go down the route of becoming banks; while banks will acquire fintechs to bring greater digital capabilities in-house. It’s going to be interesting to see how this story of fintech competition plays out.